Crypto As Junk Equity: A Mental Model

You've undoubtedly heard someone say Crypto is Junk: they probably didn't know the Junk financing market is TRILLIONS of dollars

The Crypto world’s revulsion of financial services is palpable. Call an Aave contributor a banker, and watch the color drain out of their face faster than Sam Bankman-Fried exiting a DeFi bet in November 2021, and understandably so. Crypto was undoubtedly the sexiest discipline of 2021 but risks becoming notorious in light of the ongoing cascade of bankruptcies and failures reminiscent of the 2008 financial crisis. The burden of notoriety was once well summarized by my senior MD at Goldman:

“Beware when sexy industries become notorious. Banking used to be a no brainer for anyone trying to live a comfortable life, but the scale of the winnings made it sexy in its day. Poor discipline, and a lack of focus led the industry’s catastrophic transition from a sexy to a notorious one. And once you’re notorious, you’re only going downhill.”

Notoriety benefits very few, and token-based cryptoeconomic systems are not among them. Remember that in the short term, markets are driven by social considerations (voting machine), but in the long run are always dominated by financial considerations (weighing machine), with the fear of missing out obscuring the time horizon. Market performance in 2022 tells us that investors took their eye off the ball. Tellingly, the number of google queries for “what is EBITDA” is up nearly 5x from June of last year. Hope those Google-rs got their answer, as it could be a long time before we see a bottom.

Many mental models emerged last year attempting to explain the explosion and staying power of token based models: mostly centered around social capital dynamics. Crypto as money (currency), as as utilities (digital commodities), and as branding (NFTs) are all compelling narratives to understand the asset class, though centered primarily around communal dynamics rather than market fundamentals. Some may argue this is purposeful, each of those frameworks avoids SEC attention under the Howey test.

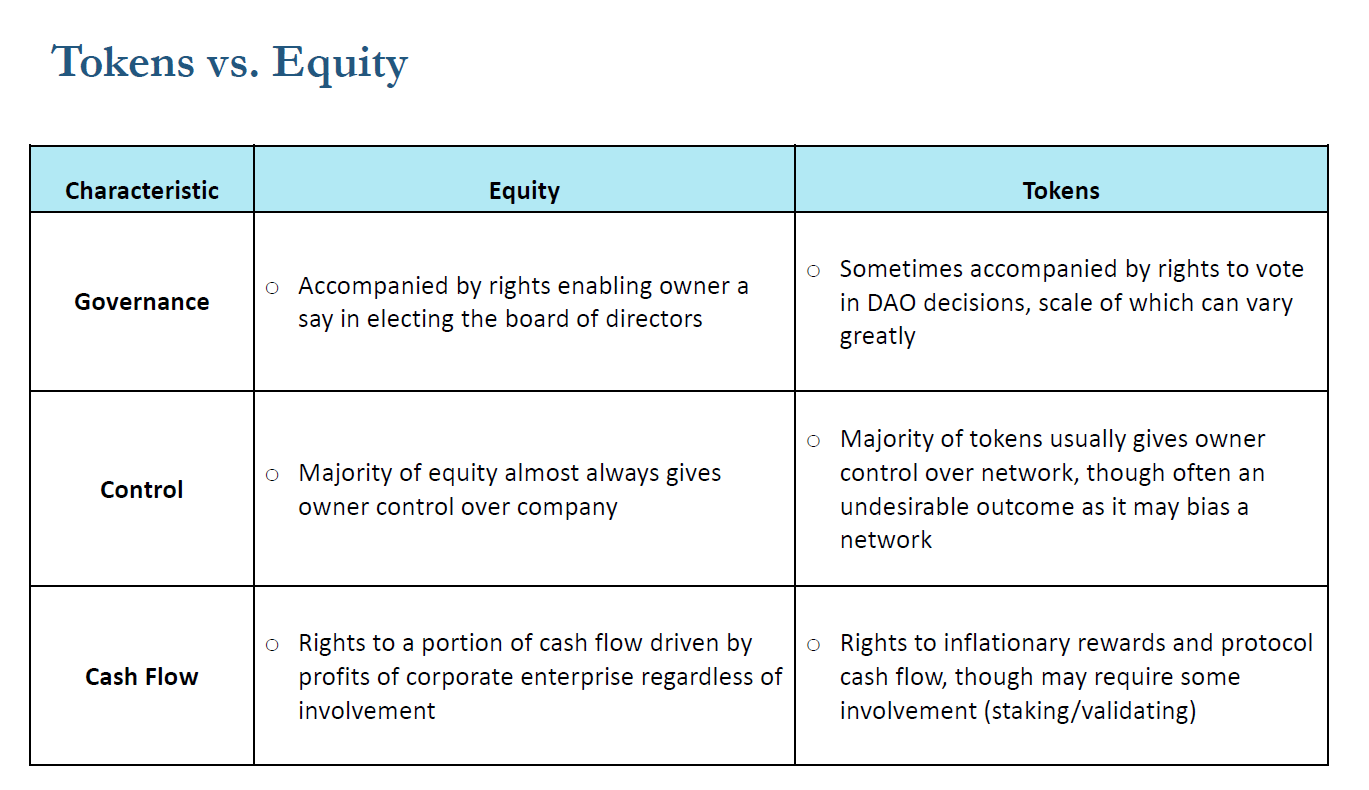

But crypto is first and foremost a financial revolution, and financial dynamics will clearly drive the future of the industry’s valuations. Cultivating the right financial mental models will separate winning and losing investors. First, we need to dig into what makes tokens and equity similar:

Using this lens, we can understand crypto as an evolution of corporate equity to a model with more flexibility and risk, less certainty and standardization, and higher expected returns. Said differently, the business models of the day encourage semi-speculative investment into assets with opaque legal rights and return profiles. While the uninformed may lose their shirt, the diligent will strike digital gold.

Given financial capital dynamics drive long-run crypto markets, we propose the junk-equity model: understanding the token’s role in the capital structure as rights-light equity. Like equity, tokens can capture residual value, but unlike equity, its rights are even more opaque and limited by design. Often the core source of cash flow is subsidy rewards funded by an inflating token, and investors must depend on token economics underpinned by incentive systems to understand the financial valuation. Understood this way, it’s less clear that tokens should be securities. There is less an expectation of profit, rather than a loose promise of return should the enterprise be successful. Simply put, tokens are skeuomorphic to equity, but there’s significantly more uncertainty around what you get.

This isn’t the first time new financing instruments have emerged that seem like lite equivalents of the existing: the debt market went through a similar revolution in the 80s, and Mike Milken ushered in the era of junk bonds. While the innocuous name junk bond may suggest this was a cordoned niche of the financial services world, junk bonds became a multi-trillion dollar asset class. Milken himself built his bank Drexel Burnham Lambert into a behemoth with ~$1.5bn of capital in 1988, before it fell apart.

Junk bonds emerged as a small group of clever financiers realized that the expansion of the fed’s balance sheet coming out of the stagflationary 70s would allow business to support more, and riskier, debt. This was more obvious to some than others: the whole debt investing industry had emerged around principles of conservatism, and few had dared to push the envelope for fear of increased losses. However, in certain moments of history, circumstance topples even universally held beliefs: the US corporate system could support more leverage than conservative thinkers honed in the 70s could comprehend. In that case, there were certain factors that make the explosion of junk bonds extremely obvious to us in retrospect including:

Balanced budget led to expansion of US balance sheet leading to lower sustained overall yields

Reconstitution of the banking system in the 70s gave borrowers more power

Emergence the “private equity” investor weaponized knowledge of financing markets

Milken’s key insight that higher yields compensated for default risk on speculative-grade companies was a powerful one, but was amplified significantly by structural innovations of the age: most notably the emergence of collateralized debt structures. The CDO was a new financing structure that multiplied bond demand many-fold, democratizing the diversification benefits of a large credit portfolio to a small firm or investor, rather than solely the large banks who were the only ones to previously benefit. With it, risky loans could be packaged together and financially engineered to “lower” the headline risk: we know in retrospect the diversification benefit was far lower than advertised given heavy correlations, but it would be years before the ultimate consequences would become clear. Structure and speculation gave way to true innovation and evolution.

Crypto today shares many characteristics with the junk bond revolution, notably facilitating the bridge between speculation and technological development. Similar to junk bonds, the crypto investment thesis is based on axioms that won’t be recognized as such for another decade, but are startlingly simple:

Financial assets are more powerful when they’re programmable

Automation and communities of motivated users can deliver better margins and asset efficiency

Trust-minimizing coordination systems operating at scale increase economic productivity

This revolution comes with its own structural evolution: the DAO, which cements decentralized ownership as a business model, and supercharges the community’s involvement in how a protocol is run. The DAO does a lot to equify tokens, creating skeuomorphic governance rights, cash flow rights, and parameters around control. DAOs bring some structure and predictability to the otherwise lawless crypto jungle, and paradigm shifts are driven by the intersection of financial and structural innovation.

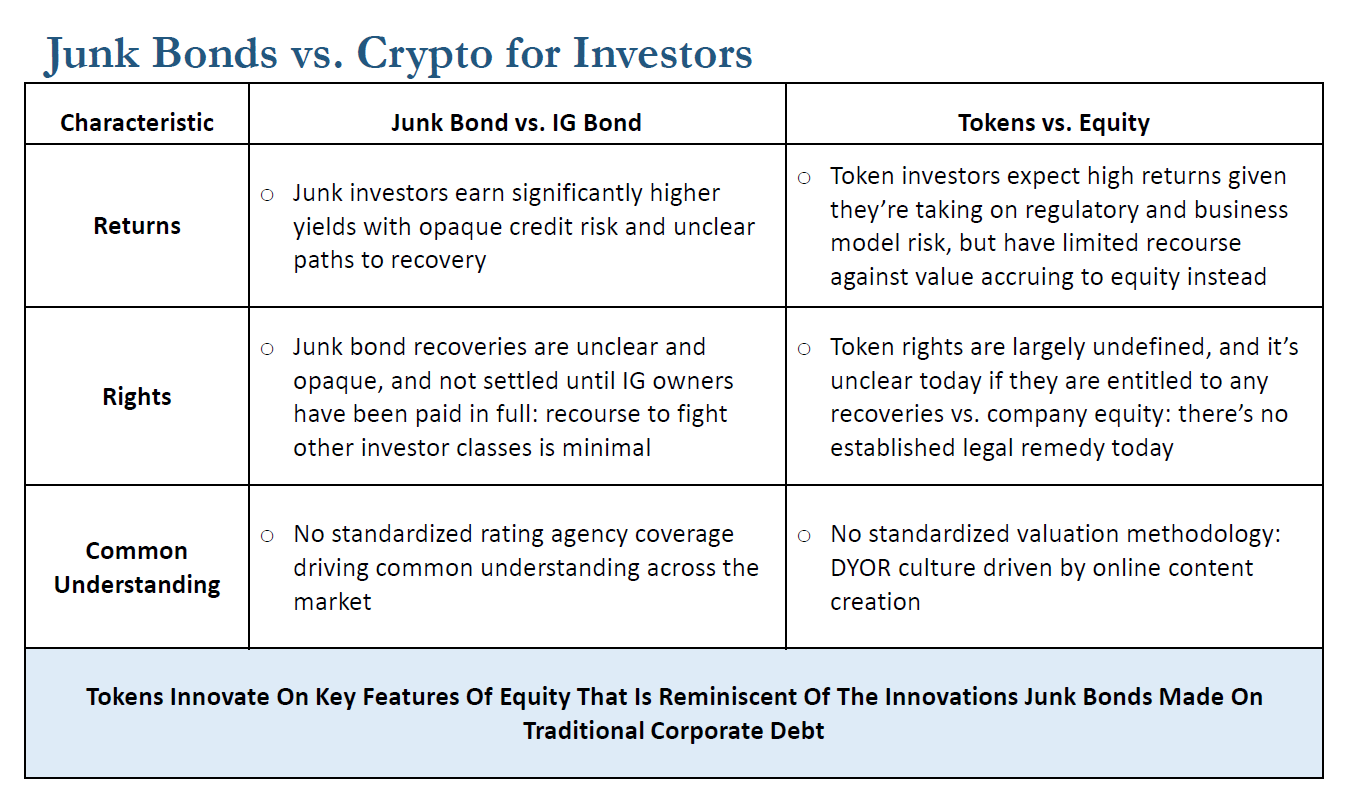

Crypto and junk bonds share many characteristics beyond encouraging speculation and innovation: they differ from their legacy counterparts in similar ways. Across return profile, investor rights, and accepted understanding, tokens strongly match the benefits and shortcomings of junk bonds.

The most important similarity between tokens and junk bonds is that they allow non-standard businesses to flourish, enabled by scaling back elements of standardization and indexation. Financial markets are extremely structured, partially driven by legacy difficulties with standard information distribution. SEC filing requirements could probably be updated to reflect the fact that people can just publish online now. The lack of structure and common understanding creates incredibly compelling opportunities for risk seeking investors to profit from their differentiated knowledge, and the lack of standardization obscures to the rest of the world what might be common understanding among those in the know. However, companies pursuing this method of junk equity financing should be very wary of Double Leverage. Your token is capitalized on your balance sheet as equity and an asset, it’s super sensitive to mark to markets. Borrowing against this “asset” which is actually a financing liability provides scope for other market participants to manipulate your asset side of the balance sheet, and force your equity negative. Lesson being, if you’re asset levered to a market traded asset, DON’T BORROW or someone external can put you under.

More than one mega alternative asset manager traces their origins to exactly this paradigm of junk financing, notably, Apollo Global Management was founded on the back of Leon Black’s use of differentiated underwriting to purchase of book of distressed junk bonds. There was no accepted framework for valuing them, so any real bid was a winning bid. Leon understood the backdrop that led to the market misunderstanding junk bonds, and bought them as quickly as possible. He rode that advantage to build the world’s second largest alternatives manager, with >$500bn+ AUM today and exceptional expertise in credit investing.

Buffet and Graham similarly pioneered the practice of investing in businesses based on working capital. What others didn’t know in the 1960s was that you could get company balance sheets from going to the SEC offices, and trade using that informational advantage. It might feel like a dirty phrase today, but rewards have always been there people who worked hard to find them in a non standard world. Once standardization enters the fray however, informational advantages are created by deception rather than grit.

We predict financially inclined token investors will outperform significantly through the next bull market, as only fundamentals can anchor an investor in the midst of the internet’s hype machine. Financial models, when implemented with extreme discipline, provide probabilistic outcomes analysis with high fidelity. Digging into token inflation models, and understanding the scale and longevity of the subsidy is an easy way to rule out bad investments (see: LooksRare). These are just companies with their finger on their lifetime equity financing source after all. Mismanagement should be as easy to spot as decisions are recorded on-chain, and markets are ruthless to take projects to zero in the case of unclear value creation. So we’ve given founders a lot more freedom in letting them control their lifetime financing, but instituted a market mechanism for valuation to let markets check wastefulness in real time. Like Junk bonds, mistakes in token structure are punished swiftly and ruthlessly, as market actors can accrue a controlling share and easily impose their will, as the Ohm protocol did to all its forks in the midst of the crash. Like Milken did in the 80s, today we’re ready to give entrepreneurs a lot more leeway en route to building a generational enterprise. But founders excited by this new paradigm should be wary that, like the aftermath of the junk bond boom, the crypto boom will also bring classes of financiers weaponizing analysis to profit significantly from pain (see Galios x Luna). And founders won’t have the benefit of white shoe lawyers with decades long understanding of institutional structure to bail them out.

Of course the Junk Equity model isn’t the right one for every situation. Tokens like ETH also conform to the crypto is money and crypto is utility models. These mental models aren’t mutually exclusive. There are however situations the Junk equity model is more applicable to: usually when a company raises both equity and token financing. For example FTX, which has a free-floating token FTT. The equity has rights to cash flow, the tokens just to a fee discount, but the token still trades at a ~$10bn diluted cap. Why? Because investors are betting that as FTX grows, parts over the business will become decentralized and begin to be governed by the token, and may even accrue cash flow. Many a corporate trained investor will look at the token and pass, but those who understand Sam’s vision know he likely will drive value to the token once we have regulatory clarity. The token is option value over the network: it’s rights-light equity.

America’s financial history is that of new, efficient markets emerging, and savvy financiers using mental models to understand their relevance before the corporate-academic illuminati arrive to justify it years later. The in between period is by definition an intensely period of higher highs, and often lower lows, as the rest of the world picks their side.

But remember, only 4% of the world owns crypto today, and it already feels like that side may be winning. Just imagine what the next billion people will do.